Loans tab

Single row, four randomized inputs.

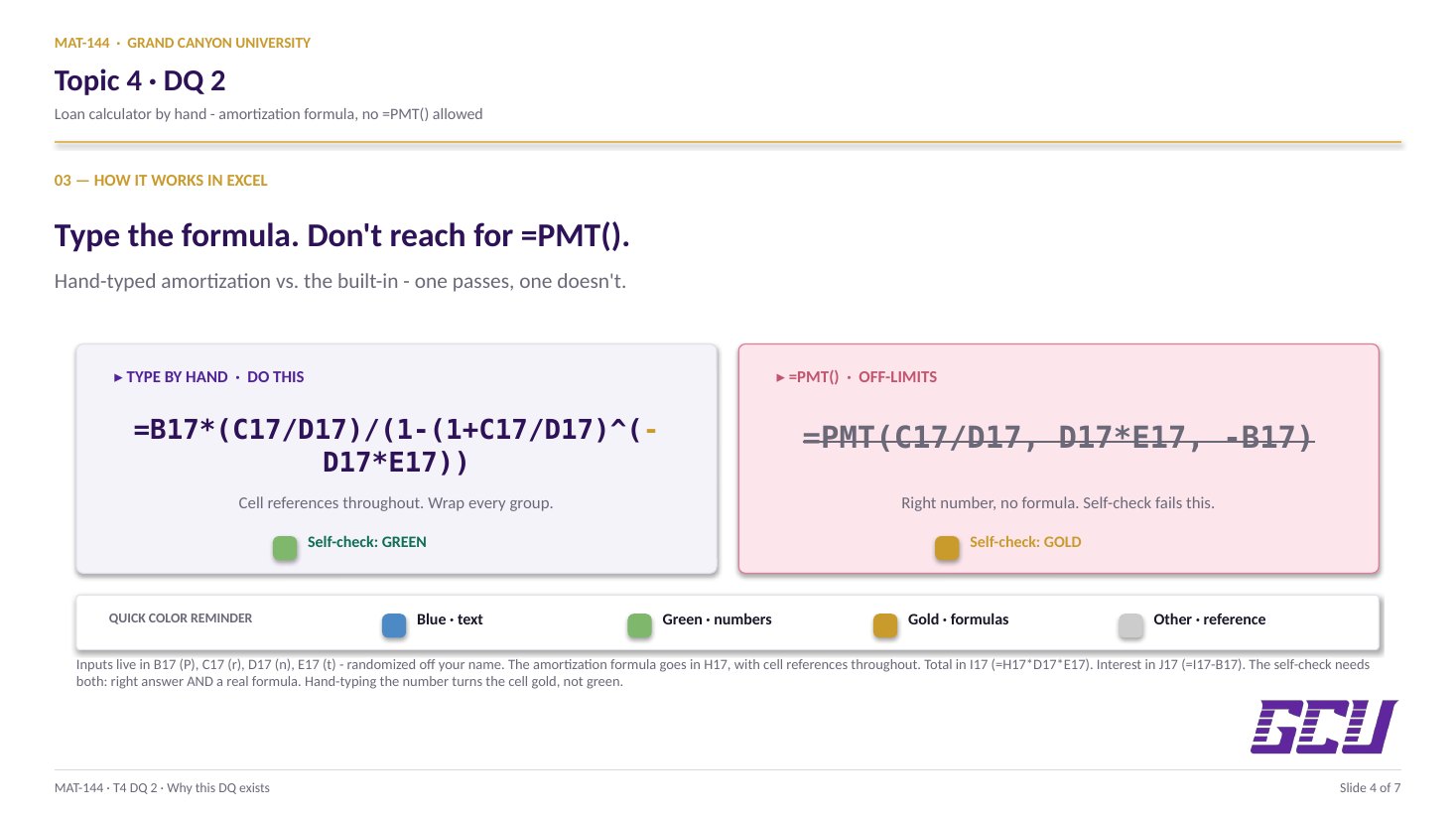

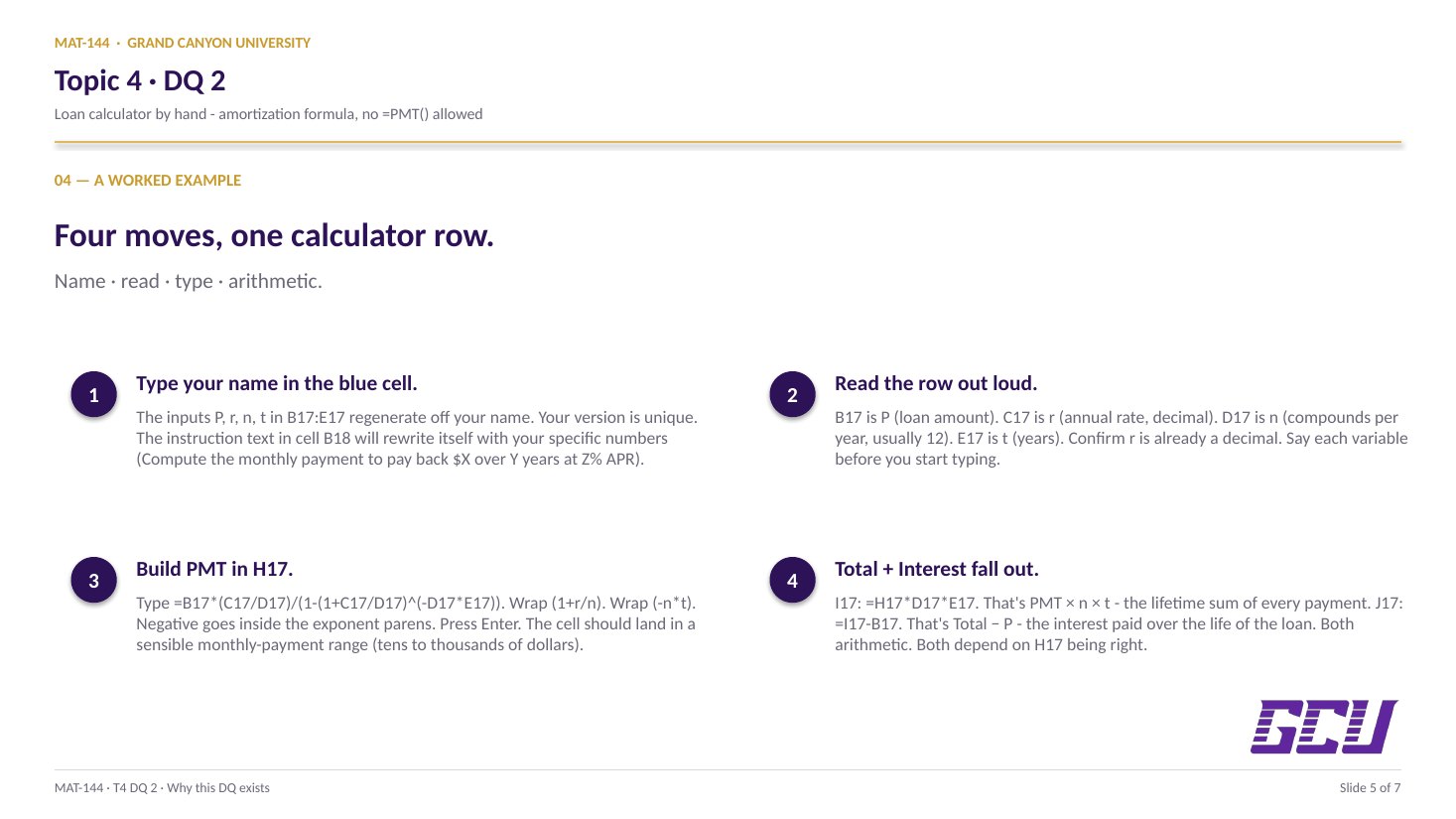

One row, four randomized inputs. The Loans tab's calculator lives at row 17. Four input cells get filled automatically based on your name (cells B17 through E17): P (loan amount), r (APR as a decimal), n (compounding periods per year), and t (term in years).

The instructions in cell B18 are a self-rendering string: once you type your name in cell C2, the prompt rewrites itself with your specific numbers, e.g. "Compute the monthly payments to pay back a loan of $X in Y years at an APR of Z." That's the problem you're solving. Three computation cells (H17, I17, J17) wait for your formulas.

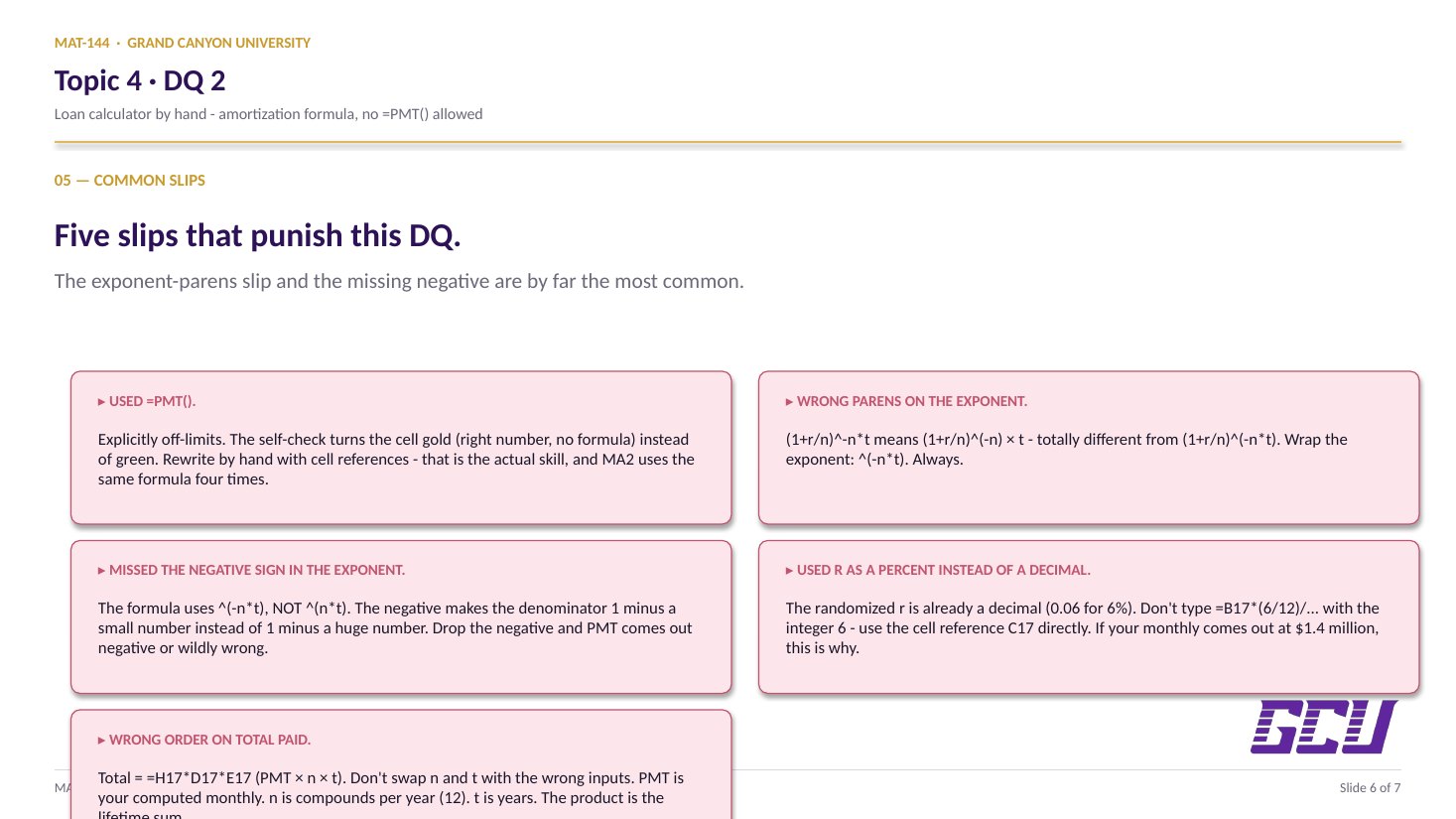

Like T3 DQ1: every student's randomized values are different, so you can't copy from a friend's sheet. The math is identical; the numbers are yours.