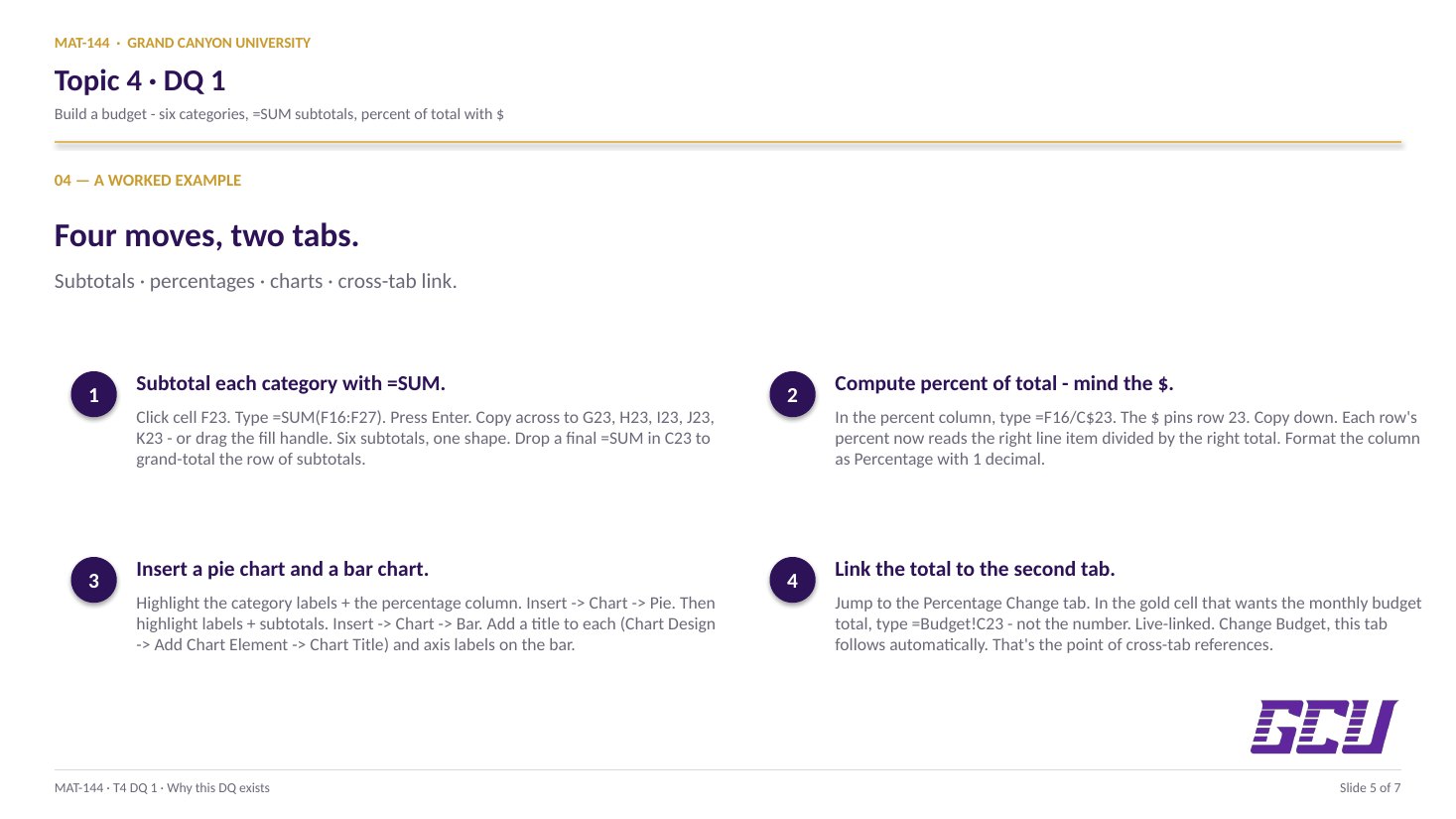

Six categories, twelve rows each.

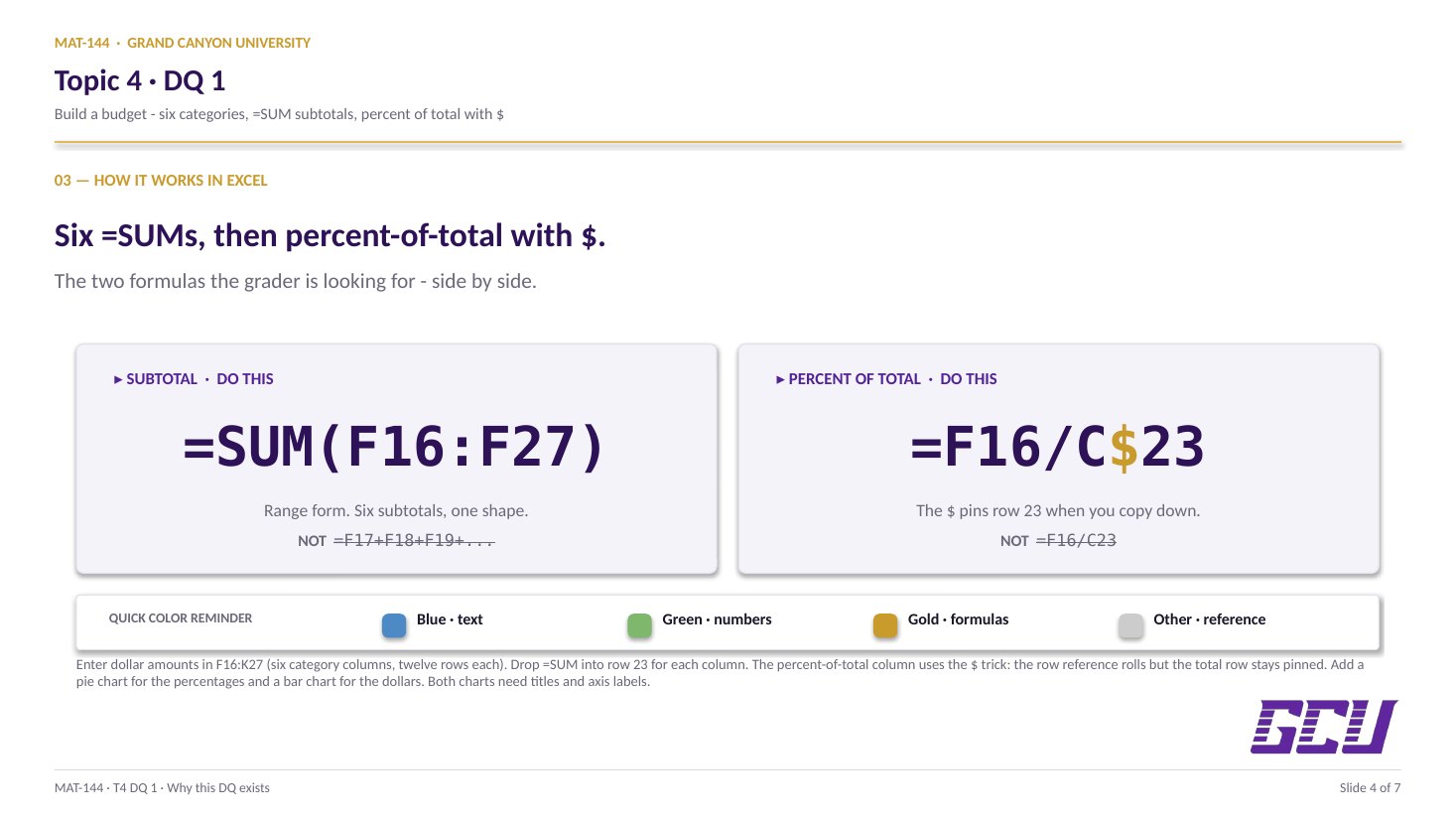

Budget tab data entry. The grid lives in columns F–K, rows 16–27. Six categories across the top — Housing, Food, Utilities, Auto, Recreation, Other — with up to twelve line-item rows under each. You enter the dollar amount for each individual expense in the appropriate cell.

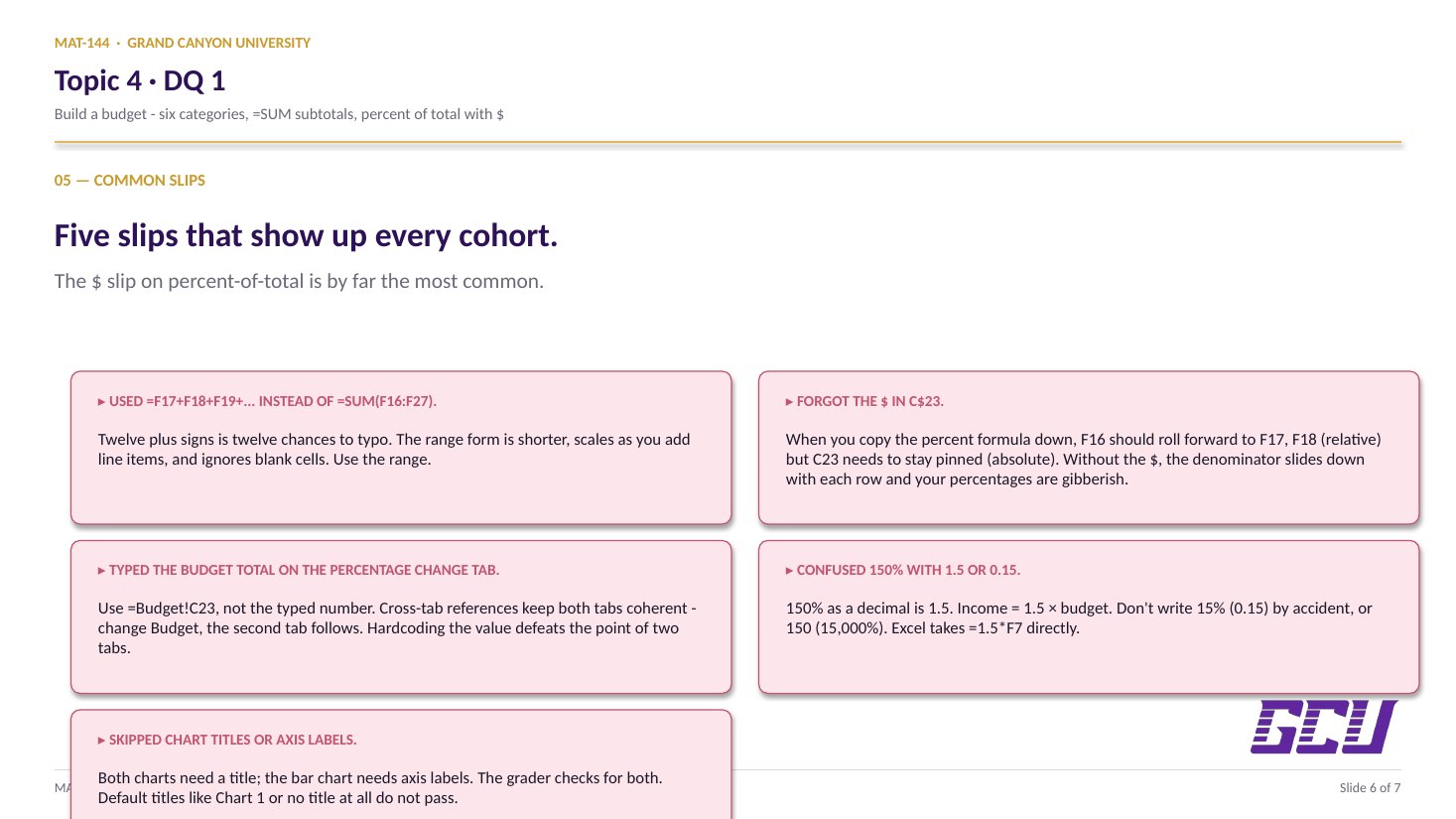

Format as currency with two decimals ($12.34, not 12.34 or $12). Use Format Cells → Currency, or just type the dollar sign as you go. The instructor's sheet will check formatting, not just values.

You don't need to fill every row. If you only have three items in Recreation, leave the other nine rows blank — the SUM formula in the next concept card handles blank cells gracefully. The reason the table goes to row 27 instead of, say, row 22 is to give you room to add line items later without breaking the formulas.