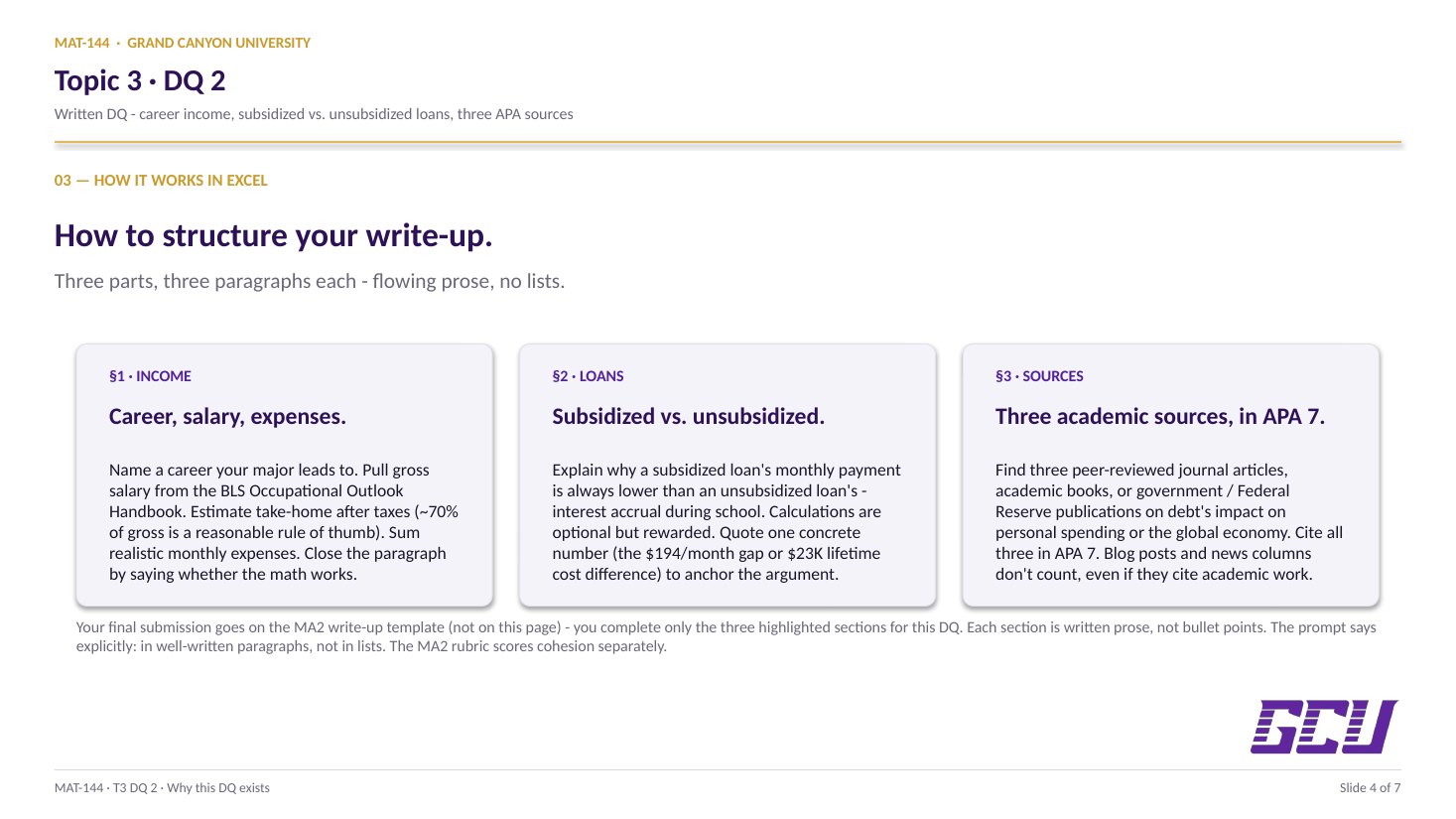

Income & expenses, three movements.

Pick a career that fits your major, then run the math from income down to what's actually left after expenses. Three movements:

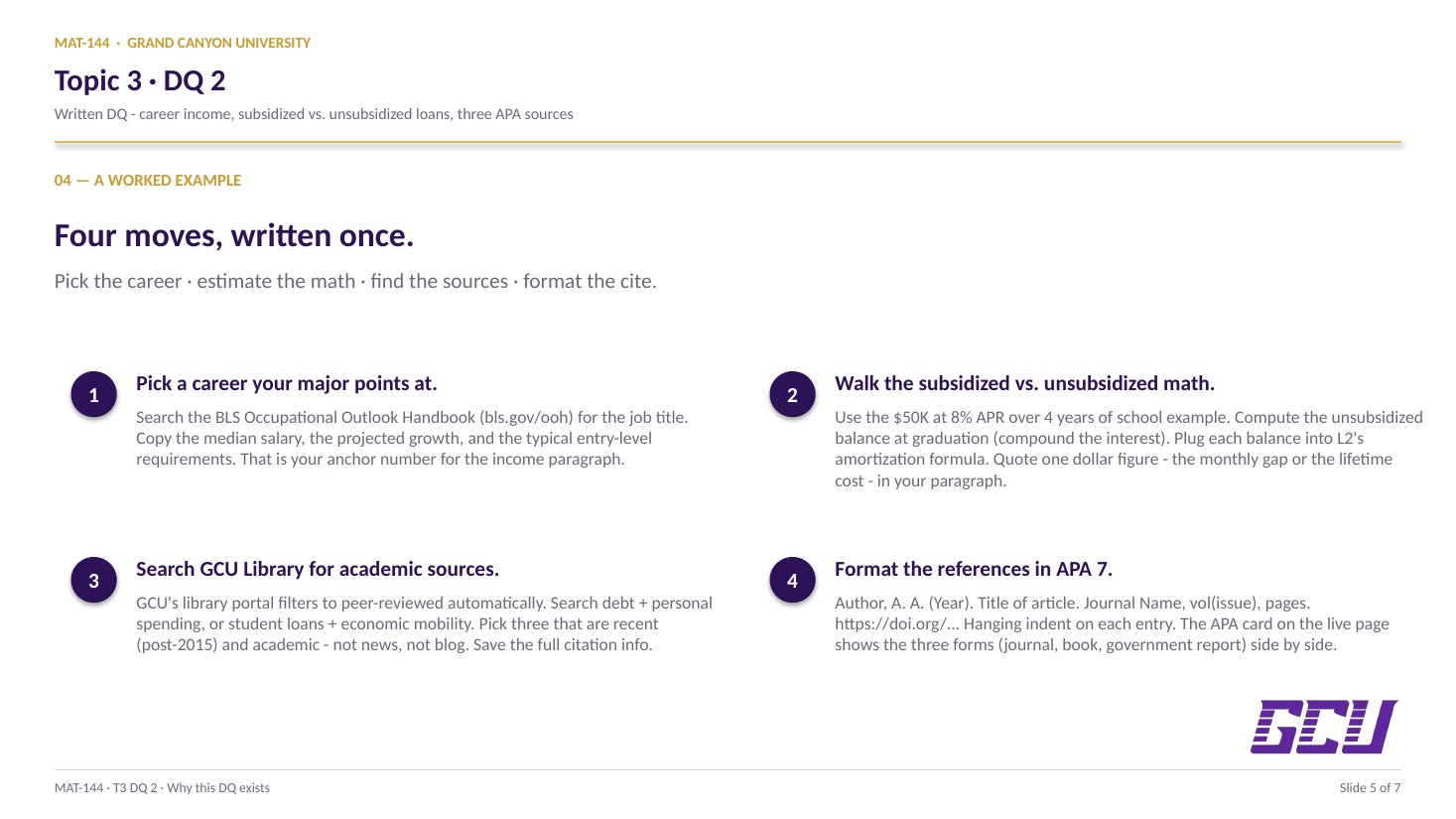

1. Find a credible salary number. The U.S.

Bureau of Labor Statistics publishes the Occupational Outlook

Handbook (bls.gov/ooh) — type your career and you

get median pay, projected job growth, and education requirements.

Cite the BLS in your write-up; round numbers from a salary site

without a credible source are easy to challenge.

2. Estimate take-home pay. Gross salary isn't what hits your account. Federal income tax, state income tax (varies — Arizona is around 2.5%), and FICA (Social Security + Medicare, ~7.65%) come out before you see a dollar. For budgeting purposes, multiply gross by 0.75 to 0.80 to estimate annual take-home; divide by 12 for monthly.

3. Compare to realistic monthly expenses. The big buckets: rent or mortgage (often the largest line), groceries, transportation (car payment + insurance + gas, or transit pass), health insurance (employer or marketplace), utilities and phone, and at minimum a small savings rate. The DQ asks for a broad estimate, not a polished budget — but the more concrete your numbers, the stronger the response.

Write this as a single flowing paragraph (the prompt is explicit about no lists). Lead with the career and salary, then walk through the deductions, end with whether the math actually works out to a livable monthly surplus.